The Income Years

Annuities

Income for the years the paycheck stops. Useful in the right spot, oversold in the wrong ones, and worth understanding before anyone shows you a brochure.

Income for the years the paycheck stops. Useful in the right spot, oversold in the wrong ones, and worth understanding before anyone shows you a brochure.

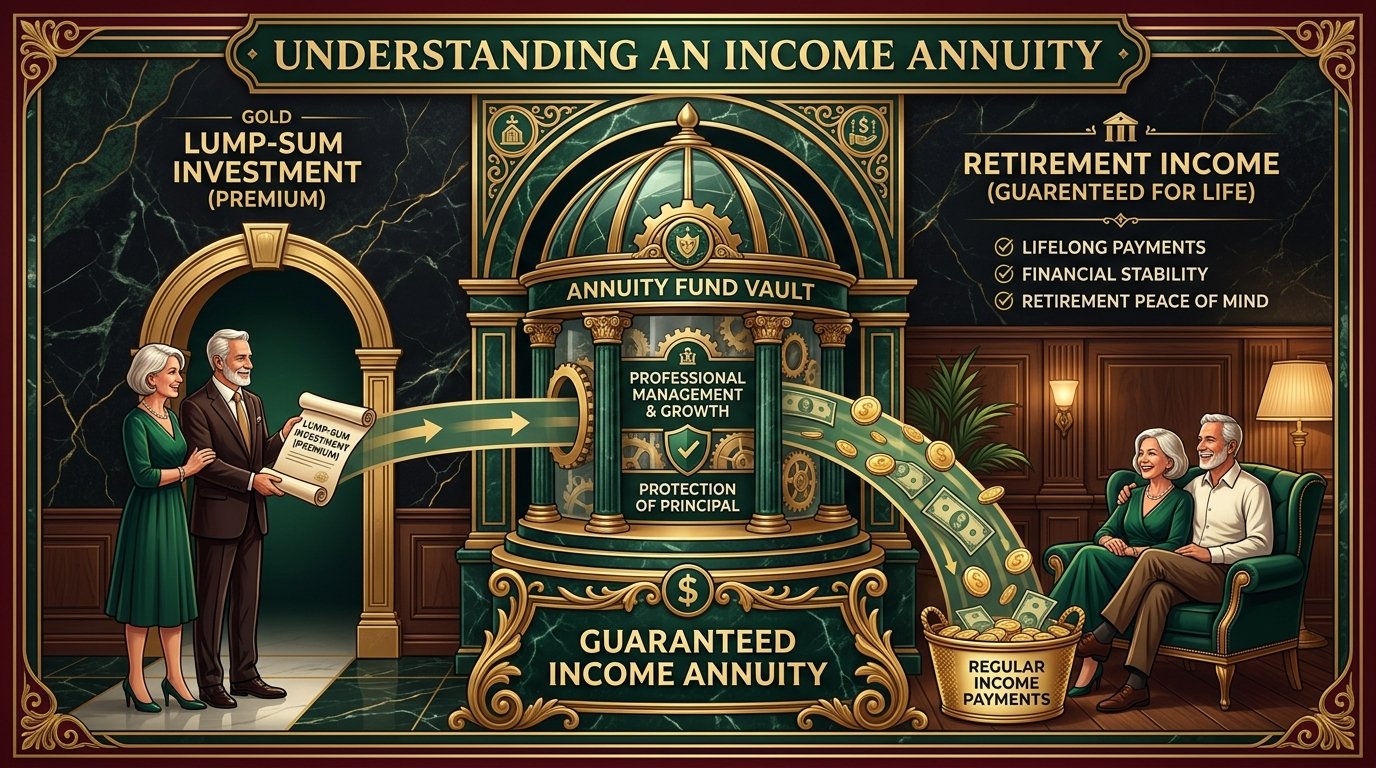

An annuity is a contract with an insurance company. You put money in, and it pays you income, starting now or years from now. Fixed annuities grow at a declared rate. Fixed indexed annuities credit interest tied to a market index with principal protection.

I own one myself, and I walk through exactly why, with the real numbers, in Why did I buy an Annuity?

Growing money and turning it into income are different problems. Once you're withdrawing in down markets, sequence matters, and guarantees start earning their keep. An annuity can cover the floor of your retirement, the income that has to show up every month, while your other assets keep handling growth.

That's a role, not a whole plan. It pairs with the retirement accounts you already own rather than replacing them.

Annuities get sold hard in this industry, and some are sold to solve the seller's problem. Surrender charges are real, liquidity is limited, and early withdrawals can cost principal and trigger taxes and penalties before 59 ½.

Get multiple opinions, and make sure whoever's selling the guarantee can explain plainly what it costs. If they can't, that's your answer.

The retirement income playlist covers what annuities are, how indexed annuities credit interest, and why I bought one, real numbers included.

Free consults for anyone. It's not a gimmick or sales ploy. We're here to help!

Schedule a Consult