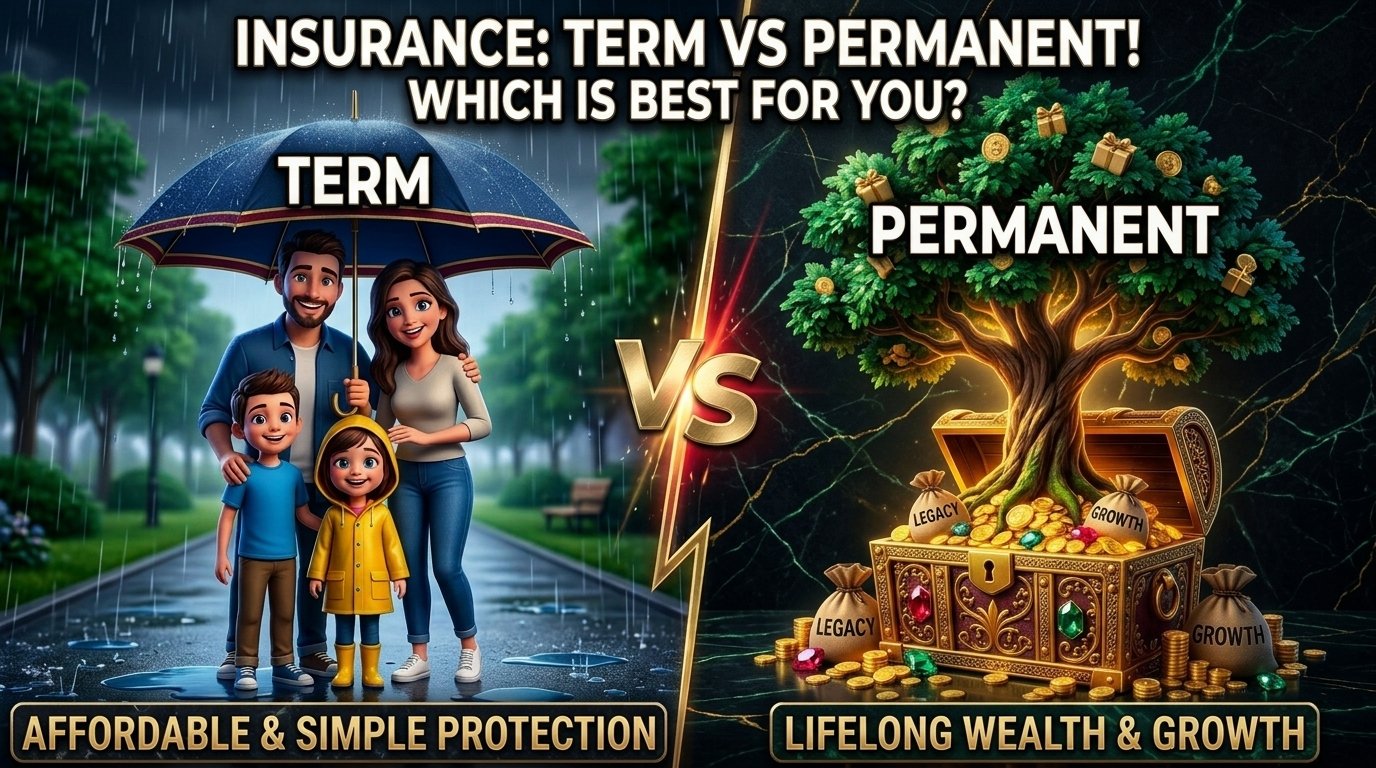

Term insurance gets honest credit here. For a young family with a mortgage and kids at home, a 20- or 30-year term policy buys a large death benefit for a small premium, and I sell plenty of it. If the budget only allows one move, cheap coverage that protects your family today generally beats expensive coverage you can't afford to keep.

The trade-off is in the name. Term covers a term. Most term policies never pay a claim, because most people outlive the window. That's not a scam, it's how the pricing works. You're renting coverage for the years the risk to your family is highest, and rent buys you nothing once the lease is up. Renew at 55 or 60 and the new premium reflects your new age, if your health still qualifies you at all.

Permanent insurance flips that trade. The premium is higher because the policy is built to pay out whenever you die, not just if you die early. And the dollar you send in does two jobs instead of one: it funds the death benefit, and it builds cash value you can generally reach while you're alive. That's the difference between renting the coverage and owning it.

Most of the families I work with end up with some of each. Term sized to the years that need the most protection, permanent sized to what the cash flow can support for life. Many term policies can convert to permanent later without a new health exam, which keeps the door open. Sizing that mix is exactly what a needs analysis is for.

Whole Life

Whole Life